05 Jun How Much Do Retired Couples Need Saved in Each State? | Nova Wealth Management

How Much Do Retired Couples Need Saved in Each State?

One of the most common retirement planning questions is simple: “How much money do I need to retire comfortably?”

The answer, however, is anything but simple.

A recent Investopedia analysis examined retirement spending across all 50 states and Washington, D.C., and found that the amount a retired couple needs can vary by more than half a million dollars depending on where they live.

According to the analysis, a typical retired couple in the United States spends approximately $84,000 annually and receives about $37,700 from Social Security benefits, leaving a gap that must be covered through savings, investments, pensions, or other income sources. Using the traditional 4% withdrawal rule, the national average nest egg needed for retirement was estimated at approximately $1.16 million.

While these numbers provide a useful benchmark, they also highlight an important reality: retirement planning is highly personal and location matters.

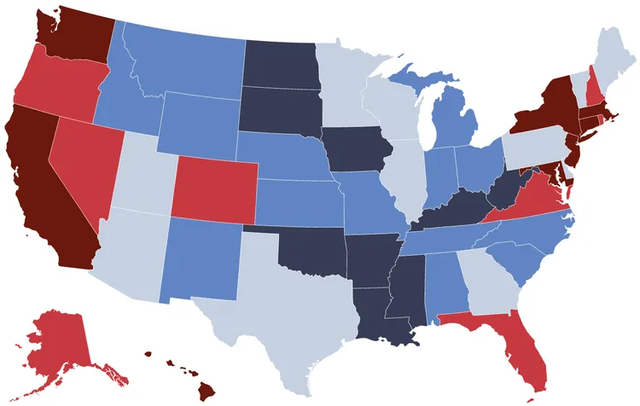

The Most Expensive States for Retired Couples

The Investopedia study identified several states where retirees may need significantly larger nest eggs to support a comfortable retirement.

The most expensive locations included:

- New Jersey – Approximately $1.33 million

- Hawaii – Approximately $1.33 million

- California – Approximately $1.32 million

- Washington, D.C. – Approximately $1.32 million

- New York – More than $1.2 million

- Washington – More than $1.2 million

- Massachusetts – More than $1.2 million

- Connecticut – More than $1.2 million

- Maryland – More than $1.2 million

Housing costs were identified as one of the primary drivers behind these higher retirement expenses.

The Most Affordable States for Retired Couples

At the other end of the spectrum, several states required significantly smaller retirement nest eggs.

The most affordable states identified in the study included:

- North Dakota – Approximately $800,000

- Arkansas – Approximately $807,000

- Mississippi – Approximately $813,000

- West Virginia – Approximately $821,000

- Iowa – Approximately $834,000

These states generally benefit from lower housing costs and lower overall living expenses compared to many coastal markets.

Retirement Planning Is About More Than a Number

While studies like this generate attention, retirement planning is about much more than reaching a specific dollar amount.

Two couples with identical account balances may experience very different retirements based on:

- Where they live

- Their spending habits

- Healthcare needs

- Taxes

- Social Security benefits

- Pension income

- Investment strategies

This is why comprehensive Retirement Income Planning often focuses on cash flow and lifestyle goals rather than simply targeting a retirement account balance.

Social Security Still Plays a Major Role

The study found that the average retired couple receives approximately $37,700 annually from Social Security benefits, covering roughly 45% of annual retirement spending. The remaining income must come from other sources.

Those sources may include:

- Traditional IRAs

- Roth IRAs

- 401(k) Plans

- Brokerage Accounts

- Pensions

- Annuities

- Investment income

Determining how and when to withdraw from these accounts can become an important part of both Retirement Tax Planning and retirement income planning.

Should You Rely on the 4% Rule?

The Investopedia analysis uses the traditional 4% rule to estimate the retirement savings needed to support spending goals.

While the 4% rule remains a useful planning guideline, retirement planning has become increasingly personalized. Factors such as longevity, inflation, market returns, healthcare costs, and tax changes may all affect how much income a portfolio can sustainably generate.

Many retirees benefit from a broader planning approach that incorporates:

- Financial Planning

- Retirement Investment Planning

- Managed Investment Accounts

- Fixed Annuities

- Money Market Accounts

- Individual Bonds

The Bottom Line

Where you retire can have a significant impact on how much you may need saved for retirement. According to Investopedia’s analysis, the difference between the least expensive and most expensive states exceeds $500,000.

However, retirement success is about more than accumulating a target account balance. A thoughtful strategy that coordinates income, investments, taxes, Social Security, and spending goals may help create greater confidence throughout retirement.

If you’d like to discuss your retirement income strategy, investment allocation, or long-term retirement goals, contact Nova Wealth Management or schedule a meeting with our team.

Source inspiration and referenced article:

Investopedia via AdvisorStream — The Typical Couple’s Cost of Retirement in Every State—And the Nest Egg You’ll Need to Afford It

Disclosure: This content is for educational purposes only and should not be construed as personalized financial, tax, or investment advice. Retirement planning strategies should be tailored to individual circumstances and objectives.

{kind=link}

{kind=link}

{kind=link}

No Comments